Development Timeline

Phased CapEx. Demand-triggered.

The current $6.5M equity raise capitalizes Phase 1 only ($20M total capitalization = $6.5M equity + $13.5M senior debt). Phase 2 and Phase 3 CapEx is demand-triggered and separately financed. The $36.5M–$48M figure is the eventual multi-phase build-out — not the current raise.

- Phase 1 · Year 0–2

RV Resort + Stage Foundation

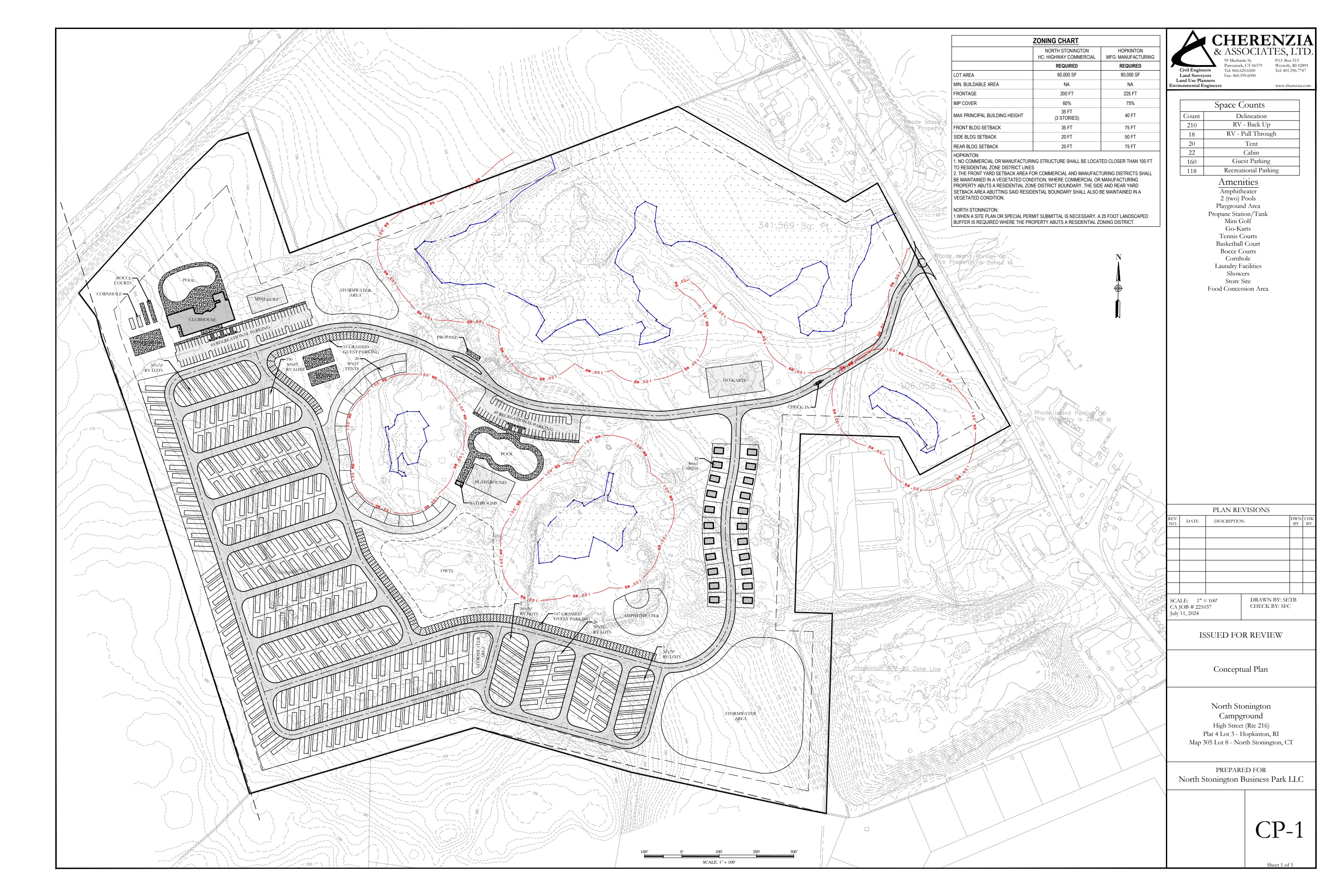

$26.0M – $33.0MLand acquisition ($3.85M), horizontal sitework, 225 RV sites (75 seasonal + 150 transient), water + septic sized for lodging-only demand, welcome center, clubhouse shell, bathhouse. Permanent stage slab, drainage, primary electrical, and FOH platform poured once, correctly — inside the septic/grading/utility envelope.

- ✓ 225 RV site nights (75 seasonal + 150 transient)

- ✓ Store / F&B / amenity fees

- ✓ Off-season RV storage

- Phase 2 · Year 2–3

Temporary Venue Activation

$0.5M – $1.0MActivate the bowl with rental-rig everything — clearspan stage roof (Mountain Productions / Stageline SAM575), sub-rented PA & lights, festival lawn seating, restroom trailers, generator power, food-truck pads on temporary utility stubs. Prove the demand thesis with two seasons of shows before pouring $10M of permanent shed concrete.

- ✓ Concert ticket sales (12–18 shows Y2, 18–24 Y3)

- ✓ Event parking ($18 × ~55% drive)

- ✓ Food truck vendor rev share (20–25%)

- ✓ Camp & Concert overnight bundles

- ✓ Initial sponsor activations

- Phase 3 · Year 4–5 (demand-triggered)

Permanent Amphitheater Build-Out

$10.0M – $14.0MTriggered only if Phase 2 proves out: ≥18 shows/yr at ≥60% paid for two consecutive seasons. Amphitheater superstructure, fixed seats + VIP boxes (~2,500 covered), permanent back-of-house, permanent concessions/restrooms, septic + water expansion to full 51K-GPD concert load, asphalt parking, mature landscaping.

- ✓ Venue naming rights (~$300–$600K/yr)

- ✓ Premium reserved + VIP box pricing

- ✓ Higher F&B per-cap with permanent kitchens

- ✓ Off-season corporate / private event rentals

- ✓ National-tour booking eligibility

- Stabilization · 2029

Year 3 Stabilized

$5.14M revenue · $2.60M NOIStabilized year-3 modeled financials: $5.14M revenue, $2.60M NOI, 2.26x DSCR. Cap-implied value at 8% = $32.5M.

- Exit · 2030

Refinance & Capital Return

Investor capital returned in fullRefinance at stabilized 8% cap; proceeds repay construction financing and return investor capital in full. Investors retain 30% ownership for ongoing cash flow + appreciation. 8% preferred return accrues throughout.

Request the full diligence package.

Land prospectus, site survey, entitlements roadmap, financial model, and operator pro forma — released under NDA to qualified investors via our secure portal.

Request Access →