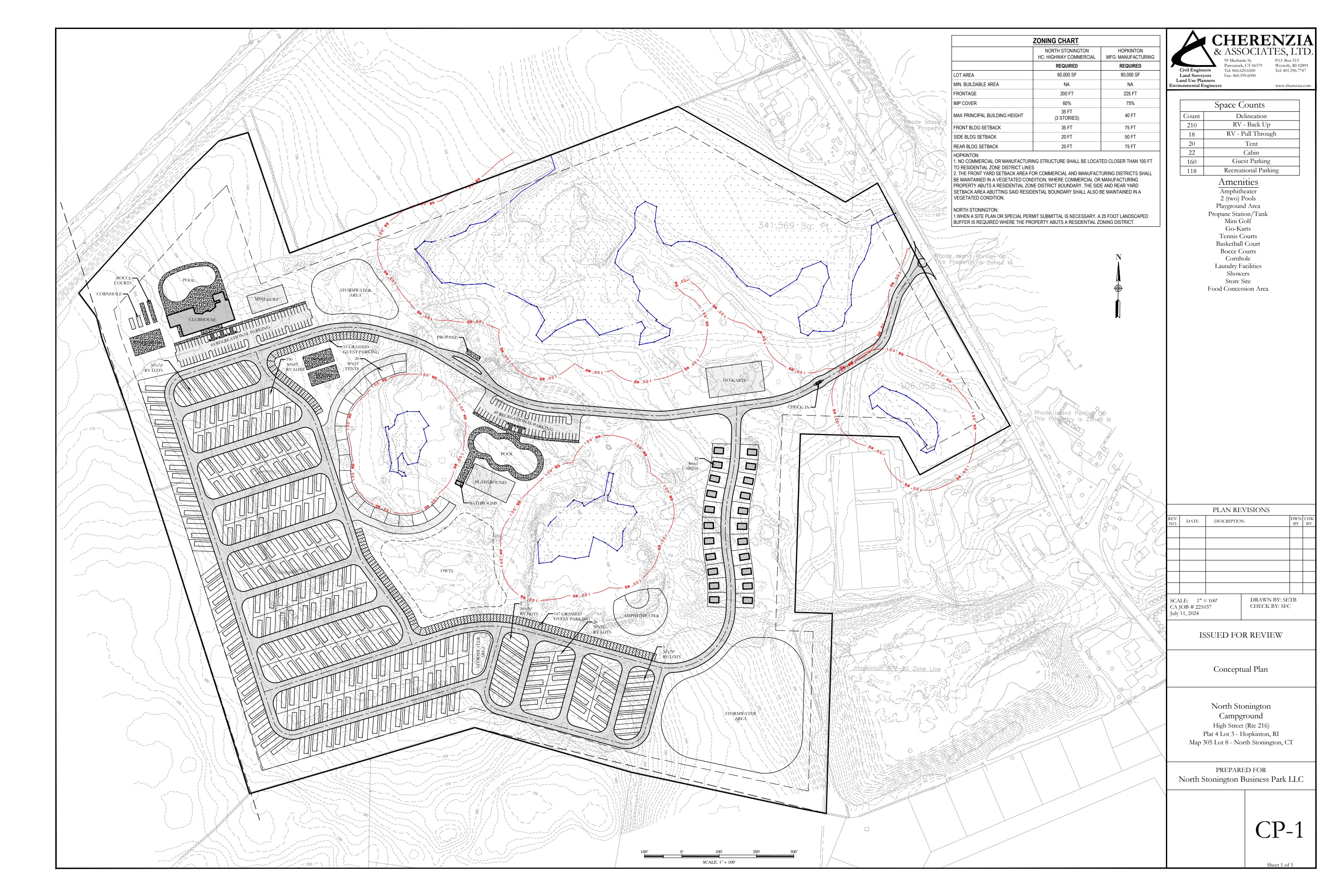

The Offering

$6.5M equity raise. $1M minimum. 8% preferred.

The offering capitalizes a $20M total project against $13.5M senior construction debt, with investor equity participating in resort NOI, amphitheater ground lease, and operator-side P&L.

Based on the approved underwriting model and projected operating assumptions.

Target investors: Family Offices · Accredited Investors · Private Equity · Hospitality Investors.

Stabilized Financials (Year 3)

$5.14M revenue. $2.60M NOI. 2.26x DSCR.

Based on the approved underwriting model and projected operating assumptions.

- Transient RV$3,163,455

- Seasonal RV$562,500

- F&B (campground)$450,000

- Camp Store$300,000

- Alcohol$250,000

- Concert-Week RV Premium$225,000

- Amphitheater Ground Lease$190,000

- Operations$700,000

- Payroll$550,000

- Mgmt Fee / GM$315,955

- Property Taxes$225,000

- Utilities$200,000

- Insurance$200,000

- Repairs$150,000

- Marketing$100,000

- Reserve$100,000

Based on the approved underwriting model and projected operating assumptions.

6-Year Pro Forma

From $3.0M opening-year revenue to $5.6M+ stabilized.

| Year | Revenue | NOI | NOI Margin |

|---|---|---|---|

| 2027 | $3.00M | $1.00M | 33.3% |

| 2028 | $4.20M | $1.90M | 45.2% |

| 2029 | $5.14M | $2.60M | 50.6% |

| 2030 | $5.30M | $2.68M | 50.6% |

| 2031 | $5.45M | $2.78M | 51.0% |

| 2032Exit | $5.60M | $2.88M | 51.4% |

Amphitheater Economics

$86 blended per-attendee, three stacked layers.

The amphitheater pays the investor in three stacked layers — the first two flow to the resort before a single ticket is sold; the third is the operator-side P&L.

$86 × 40,000 paid attendees (20 shows × 2,000 paid) = $3.44M season revenue against $2.75M season opex = $694K standalone net profit (base case, 80% paid).

Headline $32.5M valuation applies the 8% cap to Resort NOI only — the venue OpCo profit is upside, not capitalized in the asset value.

| Scenario | Paid % | Att./Show | Season Rev | Season Cost | Season Profit |

|---|---|---|---|---|---|

| Sellout | 100% | 2,500 | $4,300,000 | $2,745,876 | $1,554,124 |

| Strong | 90% | 2,250 | $3,870,000 | $2,745,876 | $1,124,124 |

| Projected (Base) | 80% | 2,000 | $3,440,000 | $2,745,876 | $694,124 |

| Break-Even | 64% | 1,597 | $2,745,894 | $2,745,876 | $18 |

Break-even sits at 64% paid — meaningfully below regional norms for a venue of this scale.

Exit & Refinance

Refinance in 2030. Return capital. Retain upside.

- 1. Refinance 2030 — proceeds repay construction financing.

- 2. Investor capital returned in full.

- 3. Investors retain 30% ownership for ongoing cash flow + appreciation.

- 4. 8% preferred return accrues throughout.

Full financial model behind the data room

Detailed projections, sensitivity tables, $86 blended per-attendee build, capital call schedule, and audited assumptions are distributed only to approved accredited investors under NDA.

Request Access

Request the full diligence package.

Land prospectus, site survey, entitlements roadmap, financial model, and operator pro forma — released under NDA to qualified investors via our secure portal.

Request Access →